Sharesies is rolling out their trial run (a.k.a beta) investments options couple weeks ago. I’ve got their invitation recently and checked out their offerings. Sharesies is currently offering six SmartShares ETFs for their investor including NZ Top 50, AUS Top 20, US 500, NZ Bond, NZ Property and AUS Resources. You can check out their current offers here.

What is Sharesies

Sharesies is a New Zealand financial start-up company supported by Kiwibank Fintech Accelerator. They are an investment platform where users can make investments with small amounts of money. One of their mission is to make investment fun, easy and affordable.

The main selling point of Sharesies is by paying a $30 annual fee, an investor can invest into multiple investments with the minimum at just $5. Also, there is a $20 credit for the early Beta investor.

Invest $5 into ETF

In comparison, SmartShares ETF initial investment is $500, set up cost is $30/ETF and monthly contribution minimum is $50. So Sharesies is a great way for beginner investor to invest in a small amount into many low-cost, diversified ETFs. It bypasses the $500 initial investment and $30 set up fee with each ETFs.

On the other hand, SuperLife also offers the same ETF in their investment fund with a different management cost. You can check out the detailed comparison here.

While Superlife also doesn’t require initial investment and the minimum contribution can be just $1. How does Sharesies stack up to SuperLife and SmartShares on ETF investing?

Sharesies vs SuperLife & SmartShares

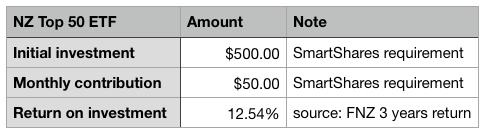

I’ve picked two popular ETF, NZ Top 50 and US 500, to run an analysis for 60 months (5 years). The analysis will compare the result on different contribution level(low and high contribution) for all three services. The low contribution will be at Sharesies minimum requirement, $30 initial investment (for the annual admin fee), $20/month contribution (about $5/week); The high contribution will be at SmartShares minimum requirement, $500 initial on each ETF, $50/month conditions.

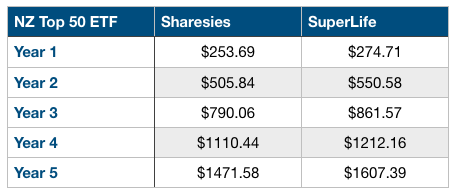

NZ Top 50 ETF at low contribution

Here is the fees structure on the ETF

This is the amount of low contribution and expected return

So Sharesies have a higher admin fee ($30) and ETF management cost (0.50%), so its expenses should be higher then Superlife NZ top 50 ETF. Since Sharesies are aiming for beginner investor, I put around $5/week as a low-level contribution. The $30 initial investment cost is to cover Sharesies annual fee. Smartshares will not be included in this analysis as the investment amount is too low.

Here is the investment return each year

Superlife did better as it has a lower management fee and admin fee resulted in a higher return for the customer. The 5-years different is $135.81, 8.4%.

NZ Top 50 ETF at high contribution

This is the amount of high contribution and expected return

We increased the contribution to $50/month, put $500 as an initial investment and include SmartShares into the mix.

Here is the investment return each year

SmartShares came out on top despite the fact that they have a higher management cost. The main reason is that Smartshares don’t have an annual admin fee while Superlife charges $1/month. However, if you wish to cash out those Smartshares at this stage, it will cost you at least $30.

The difference between SmartShares and Sharesies is $163.34, 3.3%. Although both services have the same management cost, Sharesies charge $30/year admin fee which brings down the balance.

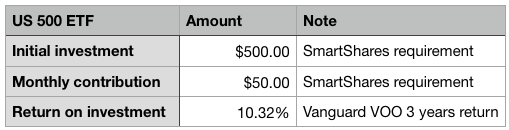

US 500 ETF at low contribution

Here is the fees structure on US 500 ETF

This is the amount of low contribution and expected return

This is more interesting as Sharesies have a lower management (0.31%) cost compare to Superlife (0.44%).

Here is the investment return each year

Due to the small amount of holding, the lower management cost (0.35%) did not cover the higher annual fee ($30) with Sharesies. Superlife holding was $122.28 more then Sharesies in year 5, 8.1%.

US 500 ETF at high contribution

This is the amount of high contribution and expected return

Now we will do the same thing by increasing the investment to Smartshares minimum requirement.

SmartShares USF came out on top with no annual fee and lower management cost. The different between SmartShares and Sharesies at year 5 is $154.75, 3.3%. The different to Superlife is $41.5, 0.9%.

In both scenario, Investor with low contribution level and better with SuperLife. If you have the $500 and $50/month to invest, SmartShares is the cheaper way. (Although I will suggest going with Superlife on NZ top 50. I’ve already covered that in another post)

How about portfolio building?

Since Sharesies investors can bypass SmartShares setup fee and initial investment requirement. So Sharesies is actually a great tool to build a simple portfolio. I will use US 500 ETF, NZ Top 50 ETF and NZ Bond ETF to build a portfolio.

Here is a balanced portfolio you can easily build with Sharesies. 25% NZ Bond, 37.5% US 500 and 37.5% NZ Top 50. If we keep the low contribution at $20/month, you can put $5 in NZ Bond, $7.5 in US 500 and $7.5 in NZ Top 50.

If you wish to set up something similar in SmartShares, you will have to spend $30 x 3 =$90 on set up fees, at least $500 x 3 = $1500 initial investment and $50 x 3 = $150/month contribution. Not feasible at all.

SuperLife, on the other hand, as my best pick for portfolio builder in New Zealand can easily build the same portfolio. Let’s check out the cost difference.

Here are the contribution and return

Here is the investment return each year

Superlife still edged out at year 5 with $123.15 more, 8.2%. I didn’t do a high contribution comparison here because SmartShares are really not fir for portfolio building.

Conclusion

Based on the analysis, SuperLife is still the better choice on low contribution and most of the high contribution (except US 500 ETF) regarding cost. However, I still think Sharesies is doing something good here.

Sharesies is promoting to young Kiwis who never invested before by providing a straightforward and easy-to-use app. The sign-up process is simple and painless. The interface is robust and delightful. They’ve done an excellent job on explaining each investment options to beginner investment and make it accessible. Check out the screenshots below.

I don’t mind about the $30 admin fee if that what’s it take for a newbie to start investing for their future. I’ve been telling readers to spend $12/year on Superlife as they have a better user interface and functions over SmartShares. Sharesies interface and user experience are way better than both of them. They made investing as easy as shopping online, which should bring a lot of people into the world of investing.

Sharesies are still in beta, so there are some functions are missing, like reinvest and auto allocation. I am sure Sharesies will continue to improve on their functions and brign in more investment options. Hope more companies like Sharesies will pop up in New Zealand to bring more people into investing.

More investor, bigger the market size, lower the cost!

Email thesmartandlazy@gmail.com or follow me on Twitter @thesmartandlazy if you have any questions.

Hi there, we are looking to invest around 10,000 for our three kids in each of their names. Just after reading this article, Do you think Superlife or Sharesies is better, and what are your thoughts on Invest Now? Many thanks!

LikeLike

Hi there, we are looking to invest around 10,000 for our three kids in each of their names. Just after reading this article, Do you think Superlife or Sharesies is better, and what are your thoughts on Invest Now? Many thanks!

LikeLike

I’ve been doing research on investing in kid’s name.

I assume your three kids are under 18. Both Superlife and Sharesies won’t accept under 18 to be on their service.

You can buy SmartShares ETF in your kids’ name, so USF and FNZ a good opinions for them. However, Smartshares is a listed pie which means everyone gets taxed at 28%. So they can’t get tax benefits on their low income.

ASB and ANZ investment will accept investing in kids name. However, their fees is not all that cheap.

InvestNow is actually a great option for kids. They will accept under 18 to be on their service. If you buy into their Vanguard fund, you will be doing the tax return on the dividend received. The kids will be paying some amount of tax as they have low income. I am planning to do for my kid and will write a blog post about it in the future.

LikeLike

That’s awesome, thank you. Yes, they’re all under 7. I’ve been looking mostly into InvestNow and am pretty happy with them especially with Vanguard. Are their any other fund providers on InvestNow that you would recommend me investigating? Just want to get a bit of a balanced fund together for the kids, ie, NZ, Aus and US. Or perhaps, should I consider investing through our family trust all in one lump sum and therefore maybe look at Simplicity as well ($15,000) I have about $5k for each child ready to invest, so I really appreciate this article you wrote!!! Awesome!

LikeLike

Well, I personally don’t think there is any other fund in InvestNow worth putting my money in….for now. InvestNow said they are getting fund from Nikko to be on InvestNow platform. I am interested in couples of their bond funds like Nikko AM NZ Bond Fund, Nikko AM NZ Corporate Bond Fund and Nikko AM Global Bond Fund. That would be ideal to mix with those Vanguard funds to create a balanced portfolio. Of course, we will need to wait and see if the cost is low enough.

Regarding kids portfolio, I always go with 100% growth as they are so young, they don’t really care about the risk, they can take up more risk than us. Anyway, that’s my personal preference.

LikeLike

Hi there, what do you think of InvestNow’s new Nikko fund fees? Still trying to make a good choice for the kids 🙂 Many thanks! Jo

LikeLike

Nikko fund fees are too high for me. Superlife bond fund charge 0.44% seems to be a better options.

LikeLiked by 1 person

PS. I Just found this on Superlife’s website… https://superlife.co.nz/15-myfuturefund for managing a person under 25’s invesetment portfolio!! So excited!

LikeLiked by 1 person

I believe that was an old offering. Last time I check they are no longer accept new account.

LikeLike

Jo, the better solution is to invest in SuperLife. greater efficiency, PIE status, greater flexibility. Look out for their product called myFutureFund. It has lower fees than Sharesies and the others mentions in Alpha’s response. It also gives better control to the parent than alternatives until the child is 25. Also beats InvestNow

LikeLike

Hi – what about simplicityfunds – how do they compare here?

LikeLike

Simplicity fund is a managed portfolio fund, so is not apple to apple when compare to Sharesies. I would say the Sharesies beta cannot build a portfolio at Simplicity level. If we try to do something similar in Sharesies, like a simplified version, it will cost more in fees.

On the other hand, Simplicity non-KiwiSaver fund initial minimum investment is $10000, so that is not a fund for beginner investor.

If you want a managed fund with low initial investment, go with SuperLife 30/60/80/100 or age step.

LikeLike

Pingback: Sharesies (Beta) – How does it stack up to SuperLife and SmartShares on ETF Investing – Kiwis pursuing Financial Independence and Retiring Early

Pingback: InvestNow Added SmartShares ETFs into their Offerings | The Smart and Lazy

SuperLife still offers the myFutureFund product and it is probably the best product in the market for saving for a child as it is very flexible, has the full range of options, low costs and fill Internet and phone App facility. It keeps the control in the hands of the parent (called a guardian) until the child is 25 and is tax efficient as it uses the child’s tax rate.

LikeLike

The last time I check was a year ago. I will call them up again. Thanks for the update.

LikeLike

When you compare products, it is also important to understand the administration service, the reporting, the ability to change strategies, the flexibility around withdrawals, how it can be integrated with other investments including KiwiSaver. You must also look at the efficiency of the investment. SuperLife invests the money the day of the contribution. There is no brokerage of lost interest while waiting to the end of the month for it to be invested.

Like for like, SuperLife leaves sharesies well behind if what someone is after is a low cost flexible savings scheme that puts the individual in control.

LikeLike

Agree, SuperLife’s function and usability are way better than Sharesies. Sharesies can only beat SuperLife at the user interface and ease-of-use.

LikeLike

Very invormative website, thanks Alpha. How do ETFs and managed PIE funds compare in your view? I invested money in Milford Unit Trust PIE Funds (mainly growth) and have been doing rather well!

LikeLike

I am not a fan of actively managed fund as I think the extra fees are not justified in the returns. They may have done well in some years but research shows its hard to find a fund that consistently beat the index. They are out there, but hard to find. All my money is in ETF or low-cost passive index fund.

LikeLike