FIRE is a movement in the personal finance space and its gaining momentum in New Zealand. We have growing numbers of Kiwis (700+) who wants to be FIRE and more people writing about it. My blog is about achieving financial freedom by being smart and lazy so FIRE is my goal. Since this is my first post in 2018, let’s start it with FIRE!

The information and idea in this blog post are primarily based on the work by Mr Money Mustache’s The Shockingly Simple Math Behind Early Retirement, Madfientist’s Shortest Path to Financial Independence and Choose FI podcast’s The Why of FI. Check out their content if you want to know more.

What is FIRE?

FIRE stands for Financial Independence Retire Early. Financial Independence means you have enough wealth to live on without working. You don’t need a job to pay for your living expenses like rent/mortgage, food, water, power as they are covered by your investment for the rest of your life. Since you don’t need a job to keep you going, you basically can retire early.

Here is an example. Let’s say your annual living expenses is $50,000/year. To maintain that lifestyle, you’ll need a job that pays about $63,000/year so your take-home pay will be around $50,000. If you have an investment portfolio worth $1.25 million and you can get 4% return after fees and tax, that 4% return is $50k. Therefore, you can live off this investment and don’t have to work as long as you can get 4% out of that investment.

(I know there is some information missing from this example and the portfolio seems really big, I will go into that later.)

Retirement is NOT an Age

The general idea for retirement in New Zealand is you work all the way from your 20s to 60s and retire when the superannuation or KiwiSaver kicks in. However, in our previous example, we can see we can use an investment portfolio to replace our job. Therefore, retirement is not really about your age. Your retirement should bebase on your investment portfolio and its return.

Use our previous example, your living expenses at $50,000 year and your take-home pay are also $50,000. So every year you spent every dollar you earned. If you having the same job and expense, you can’t really retire if you hit your 60s because New Zealand Superannuation only covers $18,729 of your expense. Therefore, you will still need to work in your 60s and 70s, or you will have some serious cut back in your retirement.

Another example, your living expenses at $50,000 year and your take-home pay are now $100,000. Now you can put away $50,000 a year to invest. You start at 25 keep saving and investing that money for 17 years. At age 42, your investment portfolio could reaches $1.25 mil. Now the investment portfolio can support that $50,000/year living expenses at 4% reture. Therefore you reach financial independence at 42 and you can retire if you want to. (You may wonder how saving and investing $50,000/year can turn into $1.25mil in 17 years. Don’t worry, I am not pulling a random number from my butt. I will cover that later.)

Now, you can see your retirement is not about your age but how much money you are invested. More importantly, you are in contorl on when and how you retire.

Typical Work Life

In typical New Zealand work life, you got out of school in your early 20s and start working. If you are really lucky, you may actually work on something you genuinely enjoy. However, for most people, we are working for the pay cheque. You may change a couple jobs along the way, and most of you will get better pay during 30s – 50s. On the other hand, our lifestyle trend to improve with our income. That’s what the society says.

During your working life, you will get your ‘first home’ with a mortgage, and then a new car, after that maybe you move up to a ‘nicer house’ and drive a ‘nicer car’ with finances. You may still manage to find some money left, why not put it as your down payment for your boat, right? Everyone is doing that! There is always stuff you can buy. Also, since you have to pay for your home, car and that boat, you need to make sure you are on top of your work so that you can enjoy your nice things during your day off.

Now you are 65 and the society says you should retire and start enjoying your life. So you go ahead and do all that fun stuff that you don’t have time to do when you are working. However, soon you will relize, you may have the money to do all those things, but you are in your 60s now. Your energy is just not the same when you are in your 30s and 40s.

Analysis that Typical work life

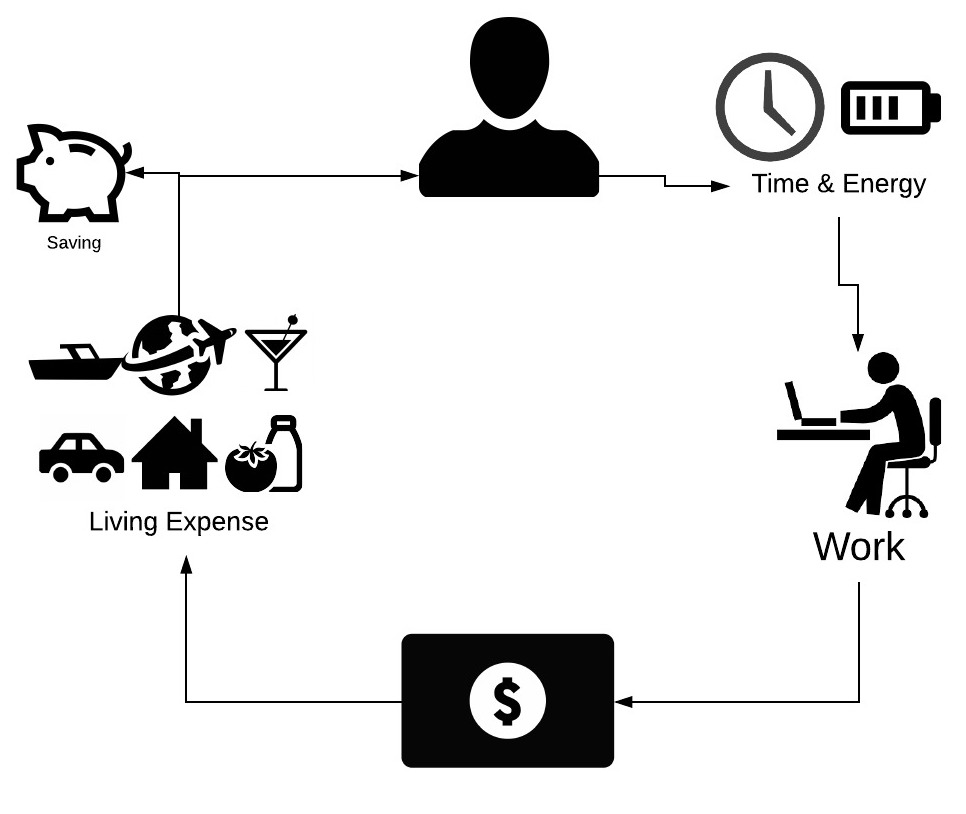

If we observe that typical work life, its basically boils down to this:

We use our time and energy to work so that we will have money. Then we that money to pay for our living expenses so we can keep working. Therefore, we are using our time and energy to support our living and maybe enjoy a bit along the way. During that cycle, we try to put a bit of money away for our retirement.

Once we hit the retirement age, we stop using our time and energy to exchange money. Instead, we will have KiwiSaver, NZ Superannuation and our retirement saving to support our living. At this point, your time and energy are running low.

It may seem sad but that is how most of the people live their life. Most of them will spend 8 hours a day, 5 days a week for a good 30-40 years working on a job that they may or may not like so they can have a typical work life that our society expects.

Set that Life on FIRE

Now that we understand most people are trading their time and energy for 30-40 years in that work life, we can start to hack it.

Here is an idea, instead of working for 30-40 years and retire at your 60s like everyone else, why not be smart and work hard for 15-20 years and retire while you still have time and energy to enjoy?

Instead of using your money to buy stuff that you may or may not need, you use that money to buy time for yourself, so you are free yourself from that loop?

Let’s look at this graph again. You need to keep working because you need the money to live and enjoy.

If we look closer on how we are spending our money, it may look like this.

We spent 40% of our income on living expenses, 35% on enjoyment and saved 5%. You may think the saving rate is low, but the data from statistics New Zealand indicate the household saving rate is actually lowered than that. That’s why most people are in this loop and working for 30-40 years is a norm in our society.

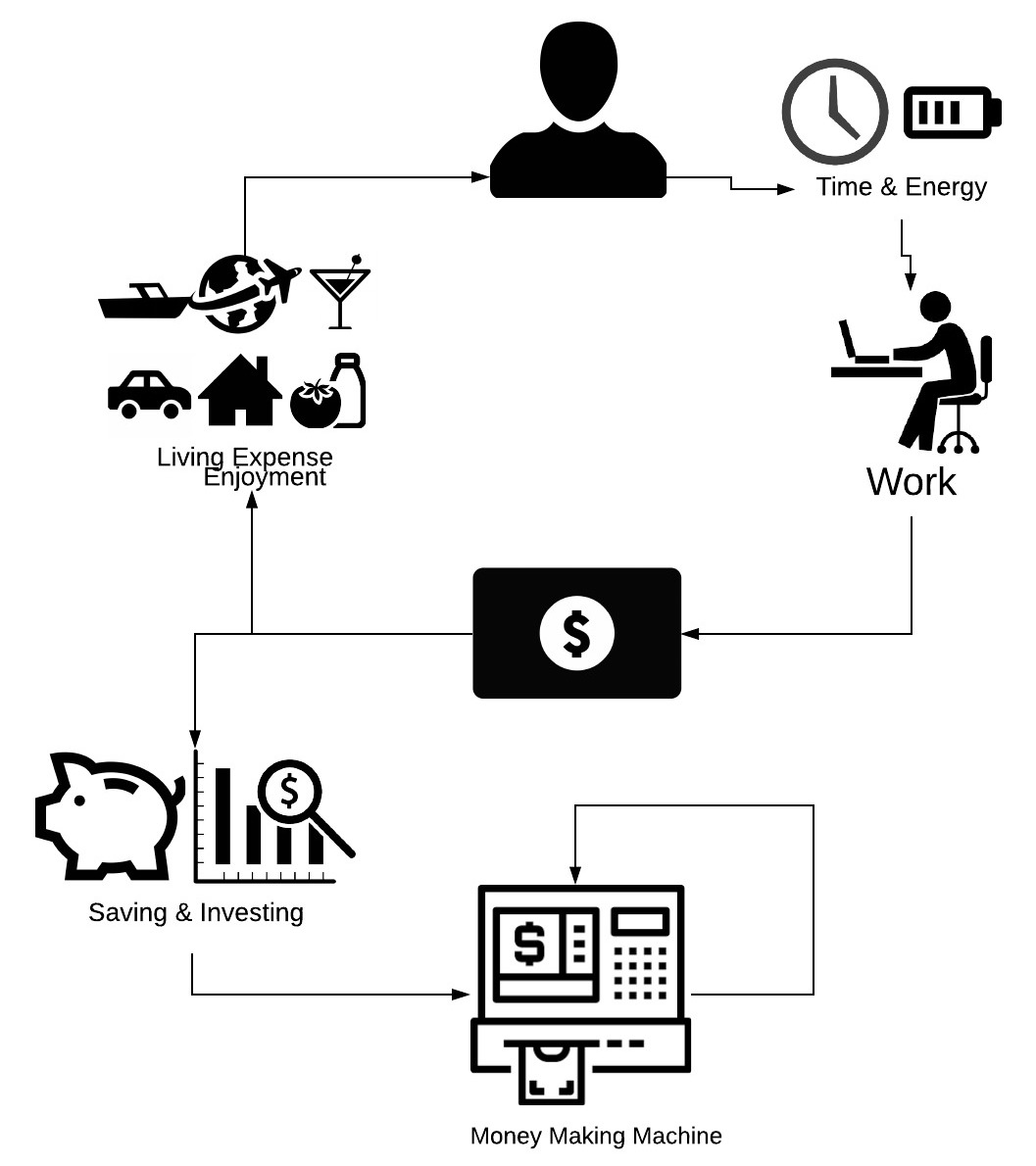

If we focus on reducing expenses on living, cut back the money spent on enjoyment and channel all disposable income into saving and investing.

Instead of buying stuff, we use our money to build a money-making-machine. That machine is your investment fund, KiwiSaver, share on the stock market, investment property and cash in the term deposit.

All of those investments in your money making machine will gain or lose money from time to time, but it should increase in value in the long run given that you invest wisely.

Once that money making machine is big enough to pay for your living expenses while leaving enough of the gains invested each year in keeping up with inflation, iIt will free you from your job.

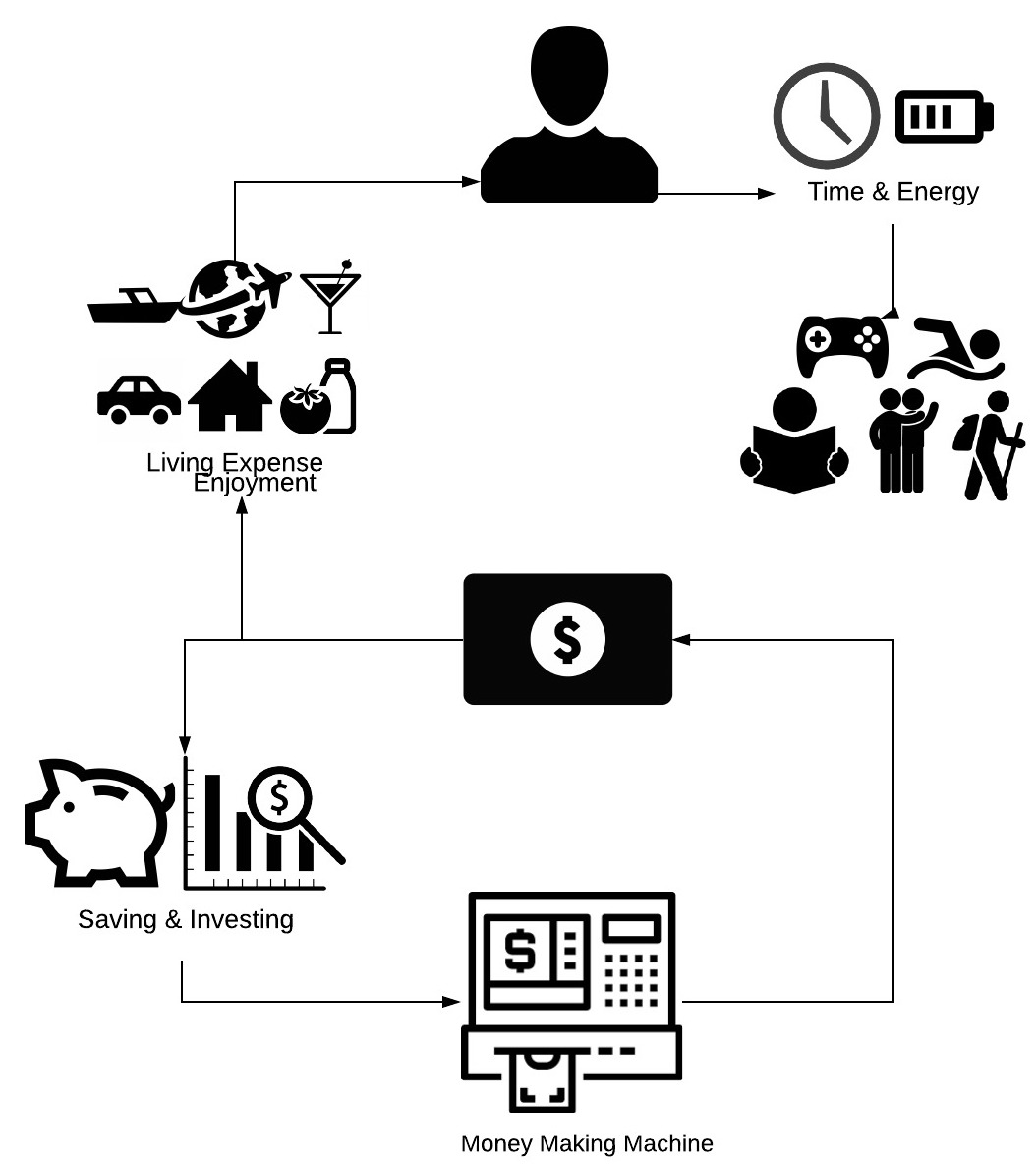

Now you can spend your time and energy to do whatever you like and don’t need to worry about living. If you like your work, you can keep working. If you don’t, you can just quit and whatever makes you happy. You are free from the loop.

Now you can spend your time and energy to do whatever you like and don’t need to worry about living. If you like your work, you can keep working. If you don’t, you can just quit and whatever makes you happy. You are free from the loop.

By the way, I like to think of my mony making machine as a machine to buy ‘time” for me, so I am investing in a time machine.

This is my money making marchine – Tardis. It’s bigger on the inside.

More to Come

I only talked about the basic idea of FIRE here. I will start to write more about FIRE in New Zealand this year. The upcoming topic includes:

- What is saving rate and how will that work out your FIRE time frame

- Wow to calculate your FIRE target and it can be a lot smaller then you imagine

- How KiwiSaver and NZ Superannuation affect your FIRE Goal

- What is Save withdraw rate

If you want to join the FIRE community in New Zealand, come and join Kiwi Mustachians facebook group. There are over 700 Kiwis who are on the path to FIRE or already reach FIRE, actively engaging in discussion regards FIRE in New Zealand.

Let’s start the FIRE now!

Real good information. We are retired and believe me you do need extra money to see one thro the retirement years.

LikeLike

Thanks for your advise. What was your biggest money surprise after retirement if you don’t mind to share?

LikeLike