Here is a frequent question from anyone who is interested in investing:

“If I put my money in XXX, how do I know if they won’t take my money and run away? What will happen to my money if XXX went out of business? Will my money go to the creditors? ”

It’s a legitimate question especially after those financial companies collapse and many kiwis loss their life saving over it. Currently, the standard practice for an investment company to protect their client’s asset is to use a custodial service. We are going to look at what is a custodian and how does it protect your investment.

I am not a legal expert so the information below could be incorrect. Always do your own research before you invest.

What is Custodian?

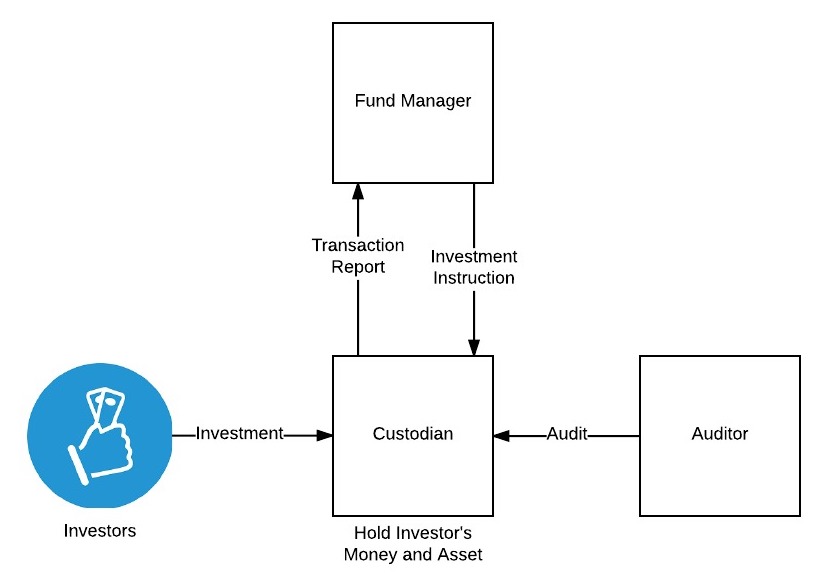

Under Financial Advisers Act, a custodian is a financial service provider who holds, transfers or makes payments with client money or property, on behalf of the client.

A custodian is required to register on Financial Service Providers Register. Their account need to be audited by a qualified auditor every year and a copy of the report will send to Financial Markets Authority. They also required reporting all client transactions at least twice a year to their client.

The custodian is usually independent of the Fund manager or investment service provider. David Campbell, former head of custody of Public Trust and current head of custody at Adminis Limited said, “Adminis holds all client assets on trust in a dedicated custody account. This ensures that there are complete separation and segregations between fund manager as a business, and their clients’ assets. This means that fund manager can’t touch or control client assets in any way.” Adminis provide custodial service for InvestNow.

Follow the Money

Lots of investors don’t know their money and investment are actually held by the custodian, not with the investment company.

For example, you decided to put $1000 in Superlife to invest in NZ Shares Fund. When you deposit the money, you are not paying into Superlife’s operation account, your money is held by their custodian, which is Public Trust. Superlife will tell Public Trust to use that $1000 and buy NZ Shares Fund. The only money goes to Superlife’s bank will be the admin fee and management fee.

The assets are held in custody, and the investor is recorded as the ‘beneficial owner’. This ensures that investor owns the asset, and also that there is complete separation of client assets from SuperLife – if SuperLife is not around, investors’ asset would still be held by the custodian, and the investor would still be recorded as the beneficial owner.

How does it Protect your Investment?

Since the fund manager and investment service provider didn’t hold investor’s asset, the asset is safe from the collapse of the fund manager.

If the investment company poorly runs, owe lots of money from different creditors and went out of business. All asset within the investment company will be sold to repay the creditors. Since the client’s asset are held by the custodian, they are a different legal entity, investment company’s creditors cannot access to their client’s money. So your investment will be safe from investment company collapse.

Also, the fund manager cannot transfer client’s name into their own bank account because they have no control over the asset. The fund manager can’t run a ponzi scam with custodian controlling the asset.

One of the largest Ponzi Scam in New Zealand – Ross Asset Managment was running by an Authorised Financial Advisers who did not use a custodial service, held all client’s asset on his own and ran a ponzi scam from his office.

Custodian is required to be audited by an independent qualified auditor annually. So it will reduce the risk of misconduct at custodian side.

What if Custodian went out of business?

You may worry if the custodian itself is poorly run and went out of business, their creditor can get their hands on your asset. Afterall, the custodian is holding your asset, right?

Not really, the custodian is actually hold their client’s asset in an another separated legal entity. It will protect your asset from custodian creditor.

Here is a real-life example. Adminis provide custodial service for InvestNow client. InvestNow’s clients’ asset is held on trust in Adminis Custodial Nominees Limited. That nominee limited does not have revenue, staff and expenses. So that company will not generate any debt and its separated from Adminis daily operation.

If Adminis goes out of business, Adminis creditors can only get Adminis’ asset, they can’t get Adminis Custodial Nominees Limited asset.

No Guarantees

Custodian is NOT a silver bullet for the financial scam, but it adds a layer of protection for investors from creditors. It makes harder for rogue fund manager or financial service provider to misplace your money and reduce the risk of misconduct.

Custodian would not protect your asset if the fund invested in junk asset or some highly speculative asset. You will still have the risk of losing your money in a bad investment decision.

If you decided to invest in a high-risk fund that focuses on cryptocurrency, and the fund manager decided to put all client money into PonziCoin. (Yes, that’s a real cryptocurrency) The custodian will use your money to invest on PonziCoin under fund manager instruction. If the PonziCoin value drops to nothing, you will lose the value of your investment. Custodian will not protect you from that. Always make sure you understand what asset you are invested in and the risk involved.

Who is using Custodian?

According to FMA, all licensed managed investment scheme managers, whether for a KiwiSaver scheme or any other type of managed investment scheme, have to ensure that a scheme’s money and property are held at arm’s length by the independent supervisor of the scheme or a custodian approved by the supervisor.

So all of your KiwiSaver providers are held under a custodian. For those non-KiwiSaver investments that I’ve been recommended from Superlife, SmartShares, InvestNow and Simplicity, they are all using independent custodian service to hold their client asset as well.

SmartShare ETF investment use custodian to hold your money for a short period of time between 20th of each month to 1st of next month. After that, they will use your money to buy the ETF, and the ETF will be under your own name.

Sharesies, the new investment start-up in Wellington, currently is not using an independent custodian service. According to section 16 of their terms and condition, Sharesies is holding investors’ asset with Sharesies Nominee Limited. That entity is separated from Sharesies Limited but fully owned by Sharesies and share the same directors.

Conclusion

- The most fund manager, KiwiSaver provider held investor’s money and asset with an independent custodian.

- An asset in held under independent custodian is separated from Fund Manager’s asset. In the event of fund manager bankruptcy, the creditors cannot access the asset under custodial control.

- It will be hard for a fund manager to misplace the fund as they don’t have direct access to their client’s money.

- Custodian is required to be audited by independent qualified auditor every year. The audit report will send to FMA.

- Custodian will further separate client asset by putting them in a non-trading nominees entity to protect from their own creditors.

- Custodian will reduce the risk of misconduct from the fund manager. It will NOT protect the investor from asset devalue.

- Always make sure you understand what asset you are invested in and the risk involved.

Special thanks to Anthony from InvestNow and David from Aminins answered some of my questions.

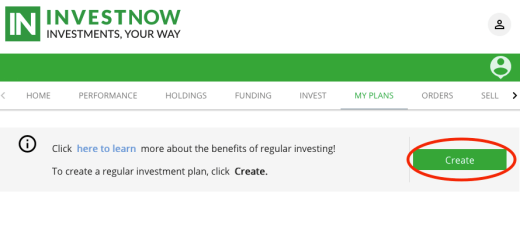

You decide how much you want to invest and how frequently. You can invest on a weekly, monthly, quarterly or six-monthly basis. Also, you can choose when the plan start and end. Below is an example for $100 invested monthly with no end date.

You decide how much you want to invest and how frequently. You can invest on a weekly, monthly, quarterly or six-monthly basis. Also, you can choose when the plan start and end. Below is an example for $100 invested monthly with no end date.