We have a sky-high house price in New Zealand at the moment, especially if you are looking to buy in major cities such as Auckland, Wellington, and Christchurch. To get your first home, you will need all the help you can get. Here comes the KiwiSaver.

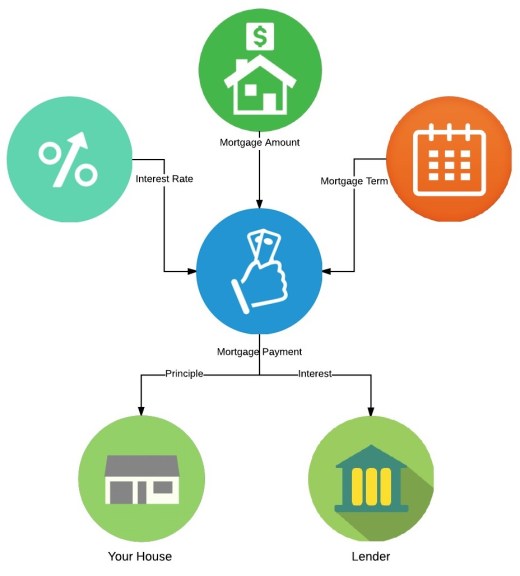

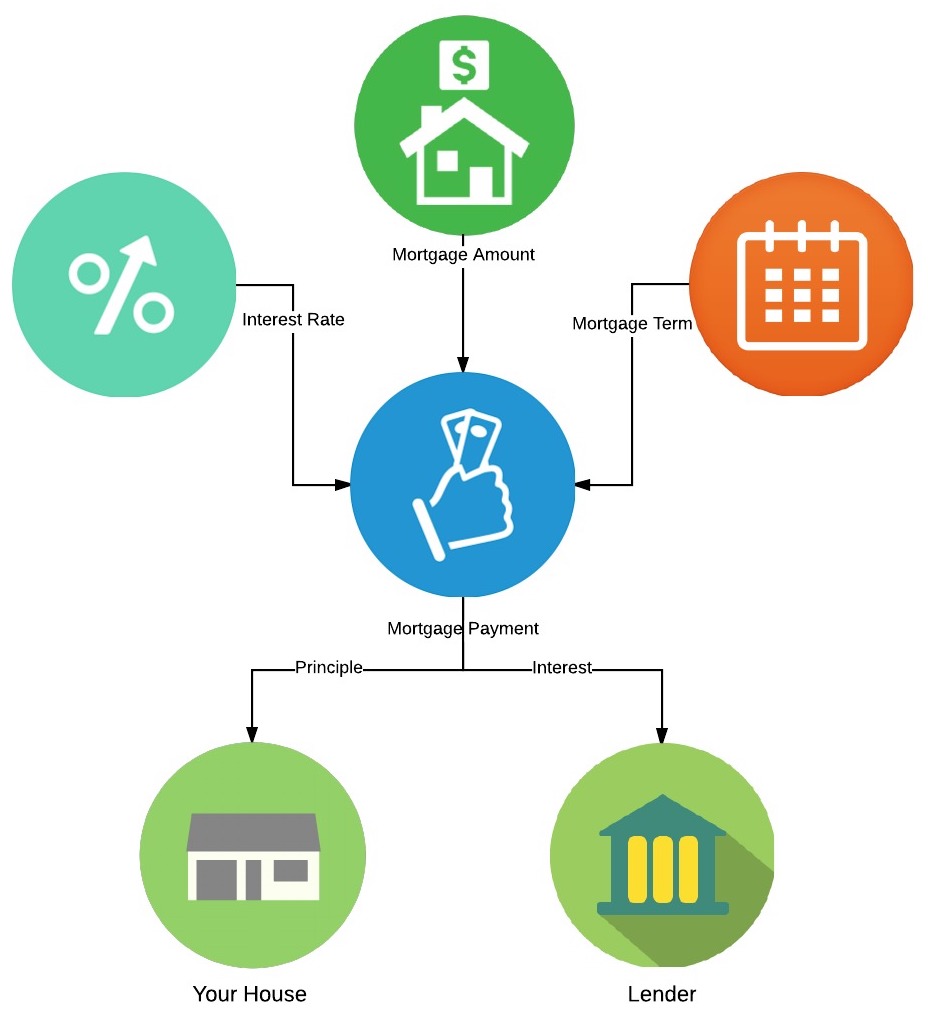

KiwiSaver First-home Withdrawal

A KiwiSaver member can withdraw most of their fund from KiwiSaver to pay for your first home. Here is the condition

- You must have been a KiwiSaver member for three or more years.

- You can ONLY withdraw money to purchase your first home – not an investment property.

- A couple can both use their KiwiSaver withdrawal on the same property as long as it is their first home.

- KiwiSaver members can withdraw most of their fund out but must leave a minimum balance of $1000 in your account.

Joe and Jill buying their First Home

Joe and Jill are a young married couple. They want to get into their first home. They’ve $65,000 cash saved up for their first home. They want to buy a $435k house in Wellington.

The $435k Dream House for Joe and Jill

To buy that house, they will need to come up with a 20% deposit. For a $435k house, they will need $435,000 x 20% = $87,000. The cash they have are not enough for a 20% deposit, but luckily, they are both in KiwiSaver. Here is their KiwiSaver balance.

- Joe joined KiwiSaver 2 years ago with the balance of $7,000.

- Jill joined KiwiSaver 10 years ago with the balance of $48,000.

Since Joe only in KiwiSaver for 2 years, he cannot withdraw his KiwiSaver balance. However, they will have enough with just Jill’s KiwiSaver.

Jill withdraw $47,000 from her KiwiSaver and left $1,000 balance in her fund. They use that money and combine with their cash, they managed to buy their first home with a mortgage.

Don’t put everything in KiwiSaver

Will and Grace also want to buy a house for $400,000. They are both in KiwiSaver for 4 years, and they were contributing 8% to KiwiSaver. They had $85,000 total in KiwiSaver and kept $10,000 in their bank. If they want to get into a $400K house with a 20% deposit, they will need $80,000. They can withdraw up to $83,000 from their KiwiSaver account.

They managed to get a $400K house from an auction (Yay!) and the real estate agent ask them for a 10% deposit on that day. Will thinks ‘No problems, I’ve got that money in my KiwiSaver.’ However, the fund in KiwiSaver can ONLY use for settlement and cannot withdraw before that. The winner of the auction is required to pay a deposit on the same day, usually at 10% of the price. So now Will and Grace need to come up with a $40,000 cheque in a short time.

Withdraw Maximum or Just Enough

I’ve got a couple readers asked about KiwiSaver First Home withdraw. One of the questions is,

Should you withdraw just enough for home deposit or withdraw maximum from your KiwiSaver?

There are good reasons for both sides of the argument. If you withdraw just enough on the KiwiSaver, more money will stay in KiwiSaver, and it will provide a better return in the future. For a 10-20 years terms, the money sitting in KiwiSaver should be averaging 6-7% return after tax and fees. Compare that to the interest of your mortgage at 4-6%, it seems better to leave the money in KiwiSaver and invest it.

On the other hand, if you withdraw all the maximum amount from KiwiSaver, you can put whatever you have as your downpayment and reduce the size of your mortgage. You can also keep same mortgage amount and have more cash on hand for emergency or home improvement.

Back let’s go back to our example of Joe and Jill and see how those two options work out. Here are the basic info and some assumption for our analysis.

House Price: $435,000

20% Deposit: $87,000

Cash on Hand: $65,000

Emergency Fund Ideal Level: $10,000

Jill’s KiwiSaver Fund Balance: $48,000

Jill’s KiwiSaver Monthly Contribution (include employer and MTC): $277.17

KiwiSaver Fund Long Term return (after tax and fees): 7%/year

Home Loan Interest rate average: 5.5%/year

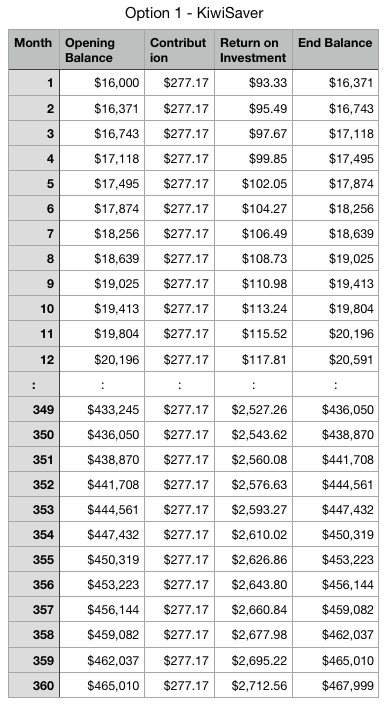

Options 1 – Withdraw just enough

They will keep $10,000 cash on hand as an emergency fund and put $55K toward the deposit. They also withdraw $32,000 from Jill’s KiwiSaver fund to make up the 20% deposit. Here is their financial breakdown

Mortgage: $348,000 (30 years term)

Minimum Mortgage payment: $1,975.91/month

Cash on hand: $10,000

Jill’s KiwiSaver Fund Balance: $16,000

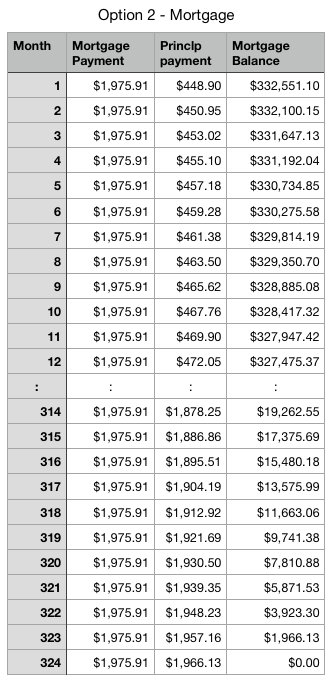

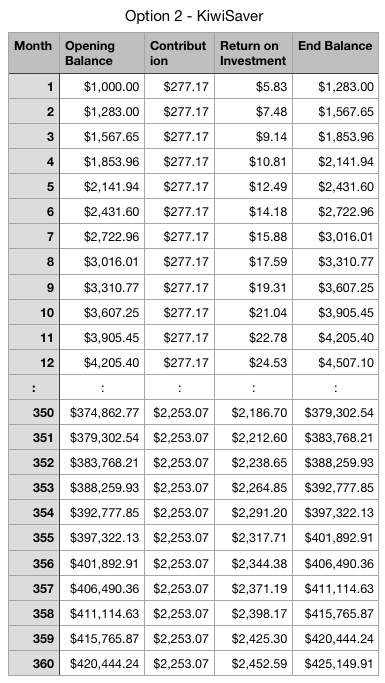

Options 2 – Withdraw maximum

They will keep $10,000 cash on hand as an emergency fund. They put their remaining cash ($55k) plus withdraw the maximum amount ($47k) from KiwiSaver toward to their downpayment ($102k). The mortgage amount will reduce to $333k, but they will pay it off as a $348k mortgage.

Mortgage: $333,000 (30 years term)

Minimum Mortgage payment: $1,890.74/month

Actual Mortgage payment: $1,975.91/month

Cash on hand: $10,000

Jill’s KiwiSaver Fund Balance: $1,000

30 Years down the road

In option 1, Joe and Jill will pay off their mortgage in 30 years while Jill’s KiwiSaver growth from $16,000. Here is the breakdown:

At the end of the 30 years, they will fully own their house, and Jill’s KiwiSaver’s balance is $468k.

In option 2, Joe and Jill will pay extra on their mortgage every month, and they will pay it off in 27 years. Once the mortgage is gone, they pay extra into the KiwiSaver.

At the end of 30 years, they fully own their house, and Jill’s KiwiSaver’s balance is $425k.

Not a clear cut answer

Based on the numbers, option 1 will have a better financial position compared to option 2. We already know that from the beginning because we set the after-tax return on KiwiSaver at 7% and mortgage interest at 5%. KiwiSaver and investing will always come out on top when you compare the number this way.

However, after I understand about risk and being a first home owner for couple years, I will prefer to reduce the mortgage (option 2).

First, there is always risk associated with investment because you’ll never know whats gonna happen. The long-term average return will be 7%, but that is based on past performance. We should keep in mind that past performance is no guarantee of future results. For all that we know, our investment maybe heading 10 years of negative returns. Also, the mortgage interest rate is not guaranteed as well. Past data shows the interest rate is at the historic low so there is real possibility it will go up. On the other hand, the return from paying off your mortgage is guaranteed and tax-free.

There is the risk in investment. Also there is the risk in life. Being a first-time homeowner with a mortgage, it will put you in a position that you’ve never been (for most people anyway) – you are DEEPLY in debt.

Before you purchase your first home, you may be someone with not much asset and a little or no debt. Once you’ve bought the house with the mortgage, you are now partly own a big asset (the lender still own the most), had a mortgage 5-15 times of your annual income, don’t have a lot of cash on hand and a big part for your income went to mortgage repayment. Financially you are in a vulnerable situation. If something happens with your life like job loss, sickness, accident or something you’ll need to fix on the house, you may be short of cash. You should avoid being in this situation by having a smaller mortgage (pay more on deposit) or have more cash on hand.

Some personal experience here. Wife and I found out we are having our first baby just 1 week after we won a house in an auction. All of our budget plans are out of the windows. We were down to one income for couple month as a new house owner. Luckily, we did one thing right on our mortgage was putting over 20% down payment on our house while the bank was advertising 5% deposit. With a bigger down payment, come with a small mortgage and a smaller minimum payment. We were managed to get through that period with careful planning and frugal living. I can’t imagine what sort of pressure we will be in if we just put down 5% deposit and borrow 95% on the house.

Based on those reasons, I personally prefer getting the maximum amount out of KiwiSaver and put it toward mortgage or keep it on hands for at least 1 year.

It’s better to withdraw Maximum

Your situation and risk appetite may be different than mine, and you may prefer to keep the money in KiwiSaver for your retirement. However, I will still recommend you withdraw the maximum amount no matter what choice you’ve made.

The reason is you can only withdraw from KiwiSaver once, but you can always put your money back in later. By having more cash when you move into a new house, it will help you to deal with any unexpected situations.

Let’s go back to our example of Jill. Jill’s KiwiSaver balance is $48K, and the maximum amount she can withdraw is $47K. She may decide to put down 20% deposit, just withdraw $32K and keep $16K in KiwiSaver for retirement (option 1).

I would suggest she still withdraw $47K out and put $40k from their cash for their 20% deposit. Now they will have $25K cash on hand and $1,000 in Jill’s KiwiSaver. She will hold on to that cash for 6-12 months to make sure their house is in order, and there is no major repair required. If everything’s fine and Jill still prefers to invest with KiwiSaver, she can put it back into her KiwiSaver after 12 months as KiwiSaver allows members to make manual contribution anytime.

How can You decide

There is a simple way to help you decide to keep the money in KiwiSaver for retirement or help reduce your mortgage.

Imagine you fully own your house today with no mortgage at all. Will you borrow $X on your house to invest in KiwiSaver for your retirement and won’t get it out until you are 67? (X is the difference between withdrawing everything and just enough. In Jill’s case, that will be $15,000.)

What I did was reserve the situation and let you look at the question from the other side. Mathematically, invest your available cash in KiwiSaver and not paying off your mortgage is the same as borrowing on your house to invest in KiwiSaver. Once I frame the question this way, you will feel the security of owning your house and the risk of investing.

Other Support from KiwiSaver

Apart from First Home Withdrawal, KiwiSaver member may be qualified for KiwiSaver HomeStart grant. Check out the information on Housing New Zealand site or contact your KiwiSaver provider.

I will continue to write more about mortgage in the coming days. There is a mortgage set up that allows the homeowner to reduce their mortgage amount while having access to cash if they need to. So stay tuned for my blog post on the Best Mortgage structure for most homeowners in New Zealand.