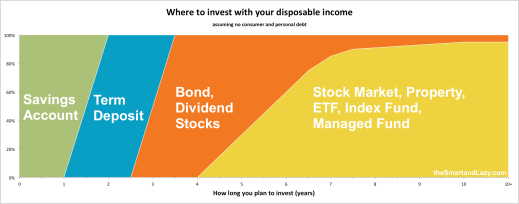

At the last post, I made a simple graph to explain where to invest your money. Now let’s break it down in more detail

Mobile-friendly version

Mobile-friendly version

Within 1 year – Cash in Savings

For such a short terms, your best bet will be keeping your money in a savings account. Most banks offer serious saver or notice saver accounts with interest around 2.25 – 2.75%. I know it’s not a good return but its better than nothing. You may also consider a 6 months to 1-year term deposit for higher interest (3 – 3.5%). However, if you need to get your money out early, you may lose the interest and pay a break fee.

Recommended products: ASB Saver Plus, ANZ Serious Saver, BNZ Rapid Save, Westpac Online Bonus Saver, Kiwi Bank Notice Saver, RaboDirect Premium Saver and Notice Saver.

2 to 3 years – Cash in Term Deposit

You still want to play it safe so you should keep the money in cash. In this time frame, you can use a term deposit as they have a higher return of interest, around 3.5 – 4%. As mentioned previously, watch out of the penalties for early termination.

Recommended products: Term Deposit for all major bank.

3 to 5 years – Income Asset (Bond and Dividend Stocks)

If your money can stay in the market for 3-5 years, income assets become a feasible opinion. BBonds are not as stable as term deposit return, but they do offer the potential to earn a higher yield. I would suggest investing in a Bond ETF or a Bond Fund over buying individual bonds via a stock broker for small investors due to the cost of trade. Bond ETFs and Funds invested in multiple corporate and government bonds, which should reduce the risk

If you are willing to dip your toes in the share market, you can buy some dividend shares at this stage. Dividend shares are usually associated with established and mature companies on the board that pays out dividends constantly. Don’t expect those companies to have rapid growth but they usually pay out dividends every quarter. The volatility of those shares is smaller compared to other shares on the market. Spark, Auckland Airport, and power companies are considered dividend stock in New Zealand.

Recommended products: NZ Bond ETF, NZ Dividend ETF, NZ Bonds Fund, Global bonds ETF, Overseas Bonds Fund.

5 to 7 years – Shares, Property, and Bond

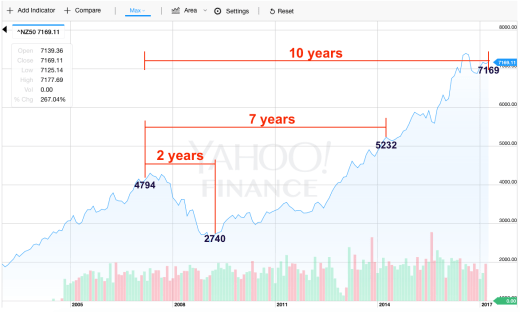

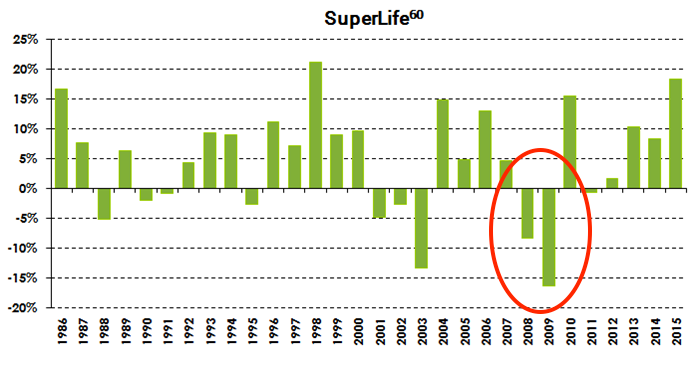

At this stage, growth assets will play an important part in your investments. Growth assets are shares, properties, and managed funds. The reason we shouldn’t touch growth assets until this stage is because of the volatility of the return. Year-to-year return can be ranged from -80% to +80% , but over longer periods it usually goes up. Take a look at the graph below. It shows the NZ stock market’s return in 2 years from April 2007 to April 2009.

If you invested in the stock market in April 2007 and planned to exit the market in April 2009, you would have lost about 35% of your investment.

On the other hand, if you had stayed in the market for 7 years, you would have gained 24% on your investment.

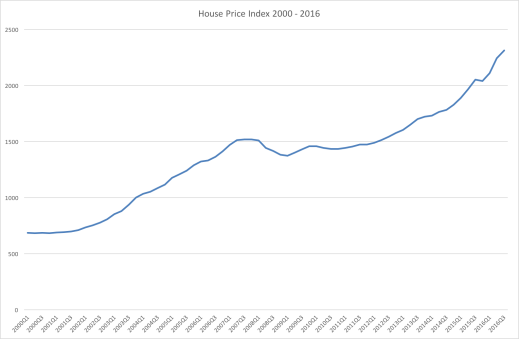

The same principle applies to property investment. The House Price index from 2000 to 2016 shows New Zealand property prices are trending up in the long term. You can see there was a dip during the 2008 GFC and the price recovered within a few years.

Therefore, in this timeframe, you should invest more and more into growth assets and the ratio of Bond and Dividend stocks should decrease.

Recommended product

30-80% of Growth Asset: NZ Top 50 ETF, S&P 500 ETF, Total World ETF, Property Fund, Oversea Shares Fund, Australian Shares Fund.

70-20% of Bond and Dividend shares.

7 years+ Mostly Growth Asset

At this point, I recommend invest 90% of your investments in growth assets and expect a long-term positive return on share and property. You may wonder why the income asset portion goes down to 10%. Although income assets are considered a safer investment, but they cannot match the high return of growth assets. Having a small amount of income assets in your investment will help offset potential downturns in your growth assets. Income assets don’t crash like growth asset, it will act as a cushion to soften any drops in the market.

Some people think if you are young and you can handle a market crash, you should have 100% growth assets as your investment. Whilst I agree with this point of view, it basically comes down to risk tolerance and personal preference.

Recommended product

90-100% of Growth Asset: NZ Top 50 ETF, S&P 500 ETF, Total World ETF, Property Fund, Oversea Shares Fund, Australian Shares Fund.

10-0% of Bond and Dividend shares.

What’s Next?

So this is the guide that I used to decide where to invest my money based on how long I was going to invest. In the next post, I will talk about risk tolerance adjustment and how KiwiSaver funds fit into this graph.

The timeline and investment ratio used in the graph are based on my own studies and conventional wisdom. Investment suggestions are based on neutral risk tolerance. Investment products listed are based on popularity, ease of access in New Zealand and a bit of personal preference.

Just a reminder, this graph is for GENERAL ADVICE ONLY. Your own situation may be different. Please thoroughly research everything you read here and seek professional advice if you need to.

Email thesmartandlazy@gmail.com or follow me on Twitter @thesmartandlazy if you have any questions.

{kind=link}