SmartShares is an excellent way to invest in low-cost, diversified ETF in New Zealand. Especially if you wish to invest in the top 500 companies on US stock market. Smartshares S&P 500 ETF (USF) is a great option for all investors as it is simple to understand, the management cost is low at 0.35% and has a long positive track record. I’ve been getting questions on how to start with investing with various investment service I covered and the most of the questions on Smartshares. So here is the guide on Smartshares.

How long will it take?

Let’s set the right expectation here, its gonna take a LONG time to set up a monthly contribution plan with SmartShares. For average Kiwi investor (without any connection to politician or United State), will take about 2-5 days to set up with most investment services. However, with SmartShares, you will have to spend around 27-53 days. Yes, that is not a typo. Just make sure you are prepared for it.

Sign up with SmartShares

We are going to walk through the setup process for an individual investing $500 into S&P 500 ETF with a $50/months contribution. Before we start, you will need to prepare the following items.

- IRD number

- NZ Drivers Licence

- Bank account number for direct debit

- Read the product disclosure statement

Go to Smartshares Invest Now page and click on “Apply online.”

Under investment options, select “Individual”, leave it blank on “Common Shareholder Number” if you are a new investor. Put $500 (minimum) on US 500 (USF) investment and $50 (minimum) as regular saving plan.

Next page is your personal information and email address. That email address will be your main point of contact. You will receive an email during the set process to confirm your email address.

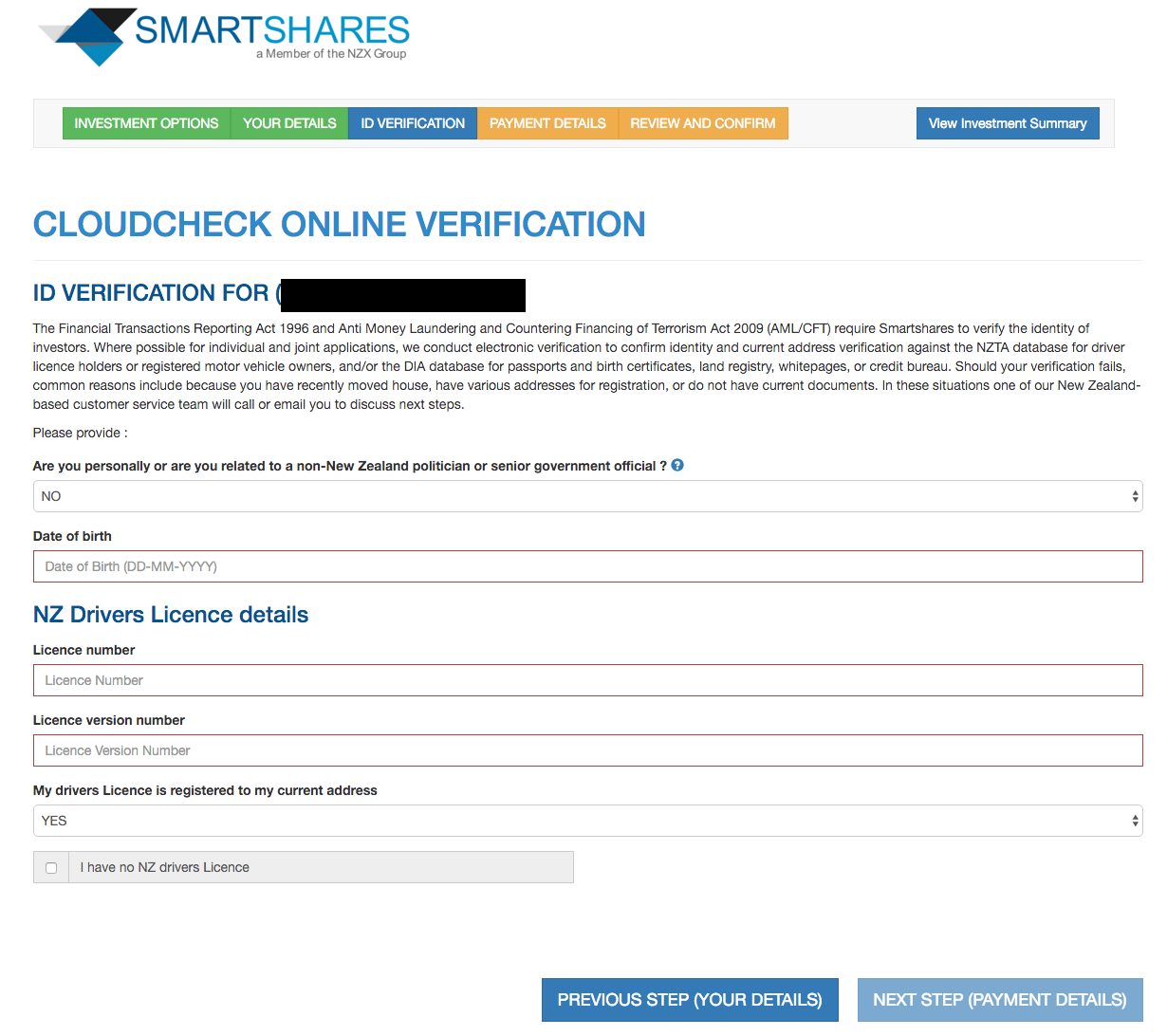

Next is your ID verification. Put in your NZ Drivers license details.

Next, confirm your payment details with your bank account no. Please make sure you have enough fund at 20th of each month.

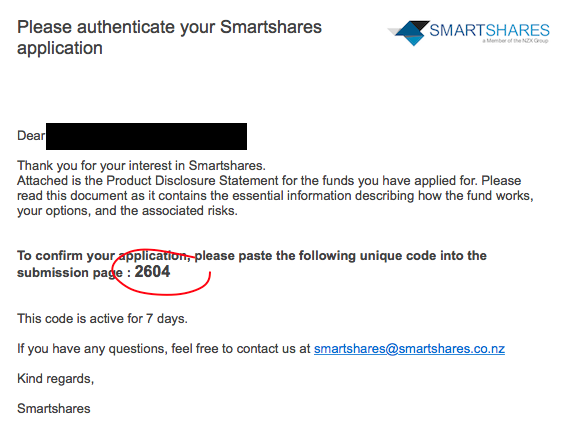

Next part you will have to review your information and confirm your contact email with an authentication code.

Here is the authentication email with the code.

Once you completed this process, you are done with the sign-up. The next part is the long wait….

What you are waiting for?

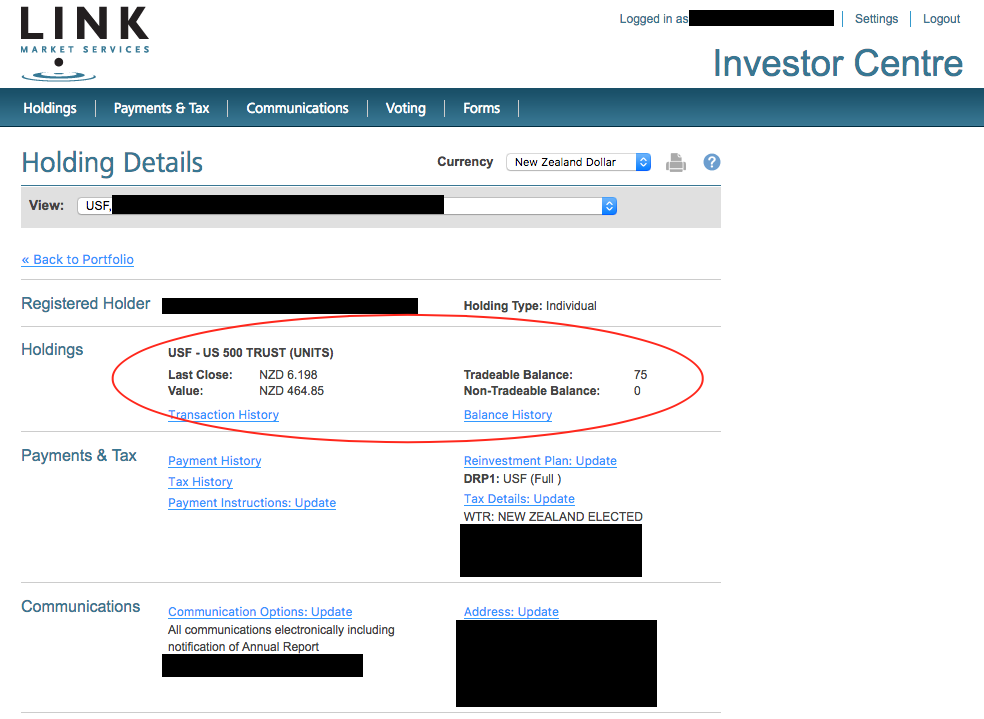

The SmartShares signup process is straightforward and painless. However, investors need to wait a long time to check up on their holding. An investor cannot log on to SmartShares to check their holding. SmartShares will direct investor to use Link Market Service to do that. To register for Link Market Service, you will need two pieces of information: FIN (Faster Identification Number) & CSN (Common Shareholder Number). FIN will send to you by mail (physical letter), and CSN will be on your holding statement in an email. You will need those two numbers to prove you own those stock. Check out this page from ANZ Securities on what is FIN and CSN.

The long wait

So here is my timeline on signing up with SmartShares.

4/5 – I submitted my application on SmartShares website.

8/5 – I got a confirmation email on my SmartShares application and my direct debit.

20/5 – $500 initial investment withdraw from my account, and it supposes to make the purchase at the beginning of June.

6/6 – the purchase happened

7/6 – a letter came into my mailbox with the FIN number. I still can’t log onto Link Market Services because I don’t have the CSN number.

12/6 – got an account statement from Link Market Service with my CSN number.

I managed to log into Link Market Service and check out my holding. Yeah!

So it took 39 days for me. To be fair, I can submit my application on 12/5 or 13/5, it will still make the 20th direct debit cut-off date. So you can shorten 7-8 days there. On the other hand, if you submit your application right after the 20th cut-off date, you will have to wait over a month.

Why it took so long?

Smartshare is NOT an investment service or fund manager. They are an ETF issuer. ETF is not an investment fund; they are tradable shares. Usually, you will have to set up a brokerage account and pay a fee to buy shares in New Zealand Stock Exchange. The minimum is $30/trade.

SmartShares offer a service allow investor buy shares in a small amount monthly without paying a brokerage fee. If I have to do it in the with a stock broker, it will cost me at least $360/year on brokerage fee alone. I am happy to wait a couple of days to save $360.

If you don’t want to wait that long, you can open up a stock brokage account and buy SmartShares directly on the stock market. It will take 2-5 days to set up a brokage account, and it will cost at least $30/trade.

Hope this blog will set an expectation for you when you sign up SmartShares. Don’t be panic when they took your money for 2 weeks without any communication. Your FIN and CSN will arrive…eventually.

{kind=link}