InvestNow announced they added 7 SmartShares ETFs into their investment platform. They are the following:

You can access to those ETFs from SmartShares, Superlife, and Sharesies (on some ETF) already. I’ve compared the cost on those ETFs on the previous post and concluded you should get most of the ETF from Superlife except US 500; SmartShares was the better choice for US 500. You can check out the related post below

Related post: Compare ETF Fund Cost between Superlife and Smartshares

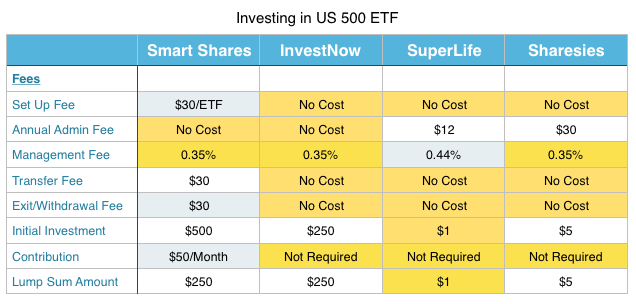

Cheapest Option for US 500 ETF

Smartshare was the cheapest option for investing in US 500 ETF because of the low management fee at 0.35% and no annual admin fee. There is a $30 set up fee if you use SmartShares contribution plan and at least $30 exit fee when you sell your ETF.

If you buy or sell the ETF on the share market, there will be $30+ transaction fee on each transaction. Superlife US 500 ETF fund has a higher management fee at 0.49% and charges a $12 annual fee. Sharesies have the same management fee with SmartShare, but they charge $30/year on admin fee. Therefore SmartShares contribution the cheapest option for US500 ETF investing.

Now InvestNow added SmartShares ETF into their offerings, it further lower the cost of US500 ETF. InvestNow offers an investment platform for investors with no annual admin fee. Investors can also bypass the $30 set up fee and the cost of exit the fund on SmartShares ETF. The minimum investment amount lower at $250 and no contribution commitment required. The management fee will be the same with SmartShares at 0.35%. Check out the comparison below. (Update: InvestNow client can now set up regular investment with just $50/transaction.)

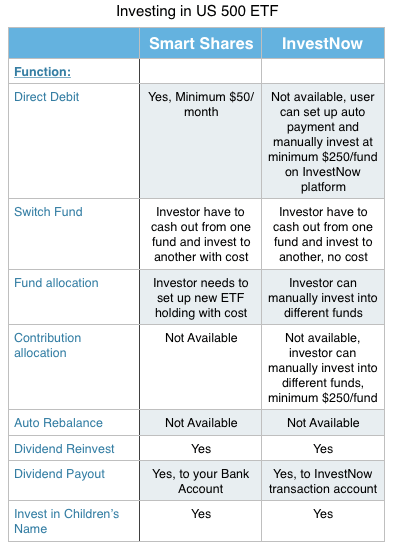

Different Way of Contribution

By looking at the number, InvestNow investors can save on $30 set up and the $30+ cost of exit, so it appears to be a better deal to SmartShares. There is a difference on how you contribute to the fund between Smartshares and InvestNow. Take a look at the function difference below.

The main limitation for InvestNow investors is the lack of small amount direct debit. SmartShares Investor will be committed to at least $50/month contribution (can be stopped at request). InvestNow investors are free to contribute whenever they want. However, the minimum contribution amount will be $250/transaction. If you only have $50/month to invest, you will have to put money in InvestNow once every five months to reach the $250 requirements. So on the one hand, you will save $30 in the beginning, but you will miss five months possible loss/return. (Update: InvestNow client can now set up regular investment with just $50/transaction.)

Compare Return Between InvestNow and SmartShares

(Update: InvestNow customer can now set up regular investment plan with just $50/transcation. InvestNow will be a better choice over SmartShares in terms of cost.)

To work out which one is the better deal on US 500, I ran an analysis to compare the return between InvestNow and SmartShares.

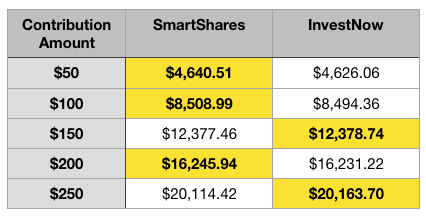

I assume the investor has $500 available to invest and can contribute $50/month. With SmartShares, the fund going to start with $470 due the to $30 setup fee and the investor will contribute $50/month. At InvestNow, investor’s fund will start with $500 and will contribute $250 every five months. The investor will continue for five years (60 months) without any withdrawal. Expected return rate is 10.32% before tax. Here is the breakdown.

Although SmarShares charge a $30 setup fee up front which lowered the starting amount to $470, they ended up with a higher end balance at $4,640.51. The reason is Smartshares investor contribute $50 every month, and those funds are growing while InvestNow customer’s money is sitting in the bank doing nothing.

Here is the result of different levels of contribution at the end of the fifth year.

SmartShares investor has a higher return over InvestNow at a lower rate, the gap close as they reach $250 marks. I stopped at $250/month because once you can contribute that amount, you can put money in InvestNow every month. From this point, InvestNow customer will always have better return over SmartShares

It seems SmartShares will be a better deal if your contribution under $200/month. However, there is a flaw in this analysis.

In my assumption, I set the rate of return at 10.32% for all five years. It assumpts the share price of the ETF going up in a straight line and investor will have a positive return every month. However, in real life share price goes up and down every day. By contributing less frequently, InvestNow investor may lose some of the gains during those five months, but they also avoid some drop as well. Afterall, the share price looks like this in real life.

Applying Real Data

So I collected the share price of US 500 ETF for the past 24 months and plugged that into our analysis. Here is the result. Click here to see the ROI.

This time InvestNow ended up with a higher balance over SmartShares. In fact, Investnow beats SmartShares on every contribution level with past data. Check out the result below.

The Real Deciding Factor

No one knows how the US 500 ETF is going to perform in the future so either service can be cheaper. If you look closely at the amount, the cost difference between InvestNow and SmartShares are insignificant, less than 0.1% of your fund. So investors will need to consider their contribution level and the experience of those two services.

In my opinion, InvestNow functions and its user interface are much better than SmartShare. InvestNow have a modern, clean and easy to understand platform. SmartShares’ holder will be checking their current stock holding on Link Market Service web site. The interface feels like it stuck in 2010.

Related post on InvestNow and SmartShares (Link Market Service)

The main limitation on InvestNow is lack direct debit option, so it’s not a “set and forget” type of investment solution. The investor will have to deposit the money into InvestNow platform and manually invest US 500 ETF on InvestNow website. InvestNow said the direct debit function is on the road map so the situation may improve in the future.

Link Market Service interface for SmartShares is not good, but you can view your holding on other services like ShareSight, Google Finance, and Yahoo Finance to improve that experience.

Conclusion

It’s great to see InvestNow adding more and more fund onto their platform. I prefer InvestNow interface and function over SmartShares. However, I understand everyone circumstances are different so here are some recommendations which service you should consider on US 500 ETF.

Use SmartShares if you want a ‘Set and Forget’ solution and you plan to contribution between $50 – $200/month.(Update: InvestNow customer can now set up regular investment plan with just $50/transcation. InvestNow will be a better choice over SmartShares in terms of cost.)- Use InvestNow if you like their user interface (you can register for free on InvestNow to check out the interface), don’t want to commit to a monthly contribution plan and happy to invest manually at minimum $250.

- Use SuperLife if you already have a portfolio with SuperLife and want to have all funds under one flexible service with great functions.

- Use Sharesies if you like their interface. Check out my comparison here.

- For other ETFs, you should use SuperLife, here is why.

Email thesmartandlazy@gmail.com or follow me on Twitter @thesmartandlazy if you have any questions.

{kind=link}

Pingback: Compare ETF Fund Cost between Superlife and Smartshares (2017 Update) | The Smart and Lazy

Pingback: Fund Update: Regular Investing with InvestNow, Cheaper SmartShares and More Funds in Sharesies | The Smart and Lazy

Pingback: New AMP Low-Cost Index Fund VS SmartShares ETF, Which one is the better deal? | The Smart and Lazy