as [I wrote this back in 5th Oct 2016]

I’ve got into a discussion with a colleague about changing KiwiSaver plan. He is in his 30s and he decided to switch his growth plan to a defensive scheme. His reasoning was that he thinks there is a market correction coming in late 2016 or the first half of 2017, so by switching to the defensive scheme, he can avoid a drop in his investment. He will switch back to growth once we are out of the correction.

I do agree there is a market correction coming and a defensive scheme will do better in a down market compared to a growth plan.

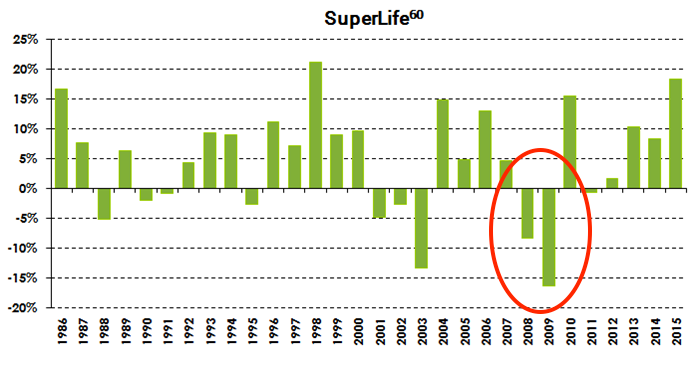

Let’s use Superlife income (defensive scheme) and Superlife60 (growth) as an example.

During the 2008 GFC, most markets were down by A LOT. SuperLife income returned about 6% to 8% during 2008-2009 and SuperLife60 was returning -8% to -14% at the same time. So if you start your Kiwisaver in 07 in SuperLife 60 (returning 4.8%), then switch to SuperLife Income at 08, 09 (6% and 8%), and finally switch back to SuperLife 60 at 2010 (15%). You would have returned on average 8.45% p.a. while SuperLife 60 was returning -0.55% in those four years.

By looking at the math, it’s all great, but the main question is HOW DO YOU KNOW WHEN TO SWITCH? We are trying to time the market. The return looks great when we do it retrospectively, but in reality, it takes lots of time, resource and knowledge to time the market and people who are experts in that area still don’t get it right. If we switch too early, we may miss out on the last bit of gain. On the other hand, if we change too late, we will take the hit of the initial crash.

I am personally not sure about this. I was trying to time the market back in 2014, and I was wrong. The conventional wisdom was to ignore the ups and downs of the market and keep your investment in a growth fund. You will ride it out eventually. However, somewhere in my mind I still think I can get a better return by switching. Not to a defensive scheme but a balanced scheme to smooth it out.

[Now, back to March 2017]

I ended up keeping the growth fund and it turned out great. The return on those months is far better than the defensive fund. The main reason was due to the poor performance of income asset in the last quarter of 2016.

However, this post is not about growth fund doing better than the defensive fund during that time period. In fact, I’d still be happy if the defensive fund did better because the performance for my KiwiSaver in a single quarter only has a tiny impact on the lifetime of my fund. The lesson I learned was to stick to right fund for me, just sit back and let it grow.

Email thesmartandlazy@gmail.com or follow me on Twitter @thesmartandlazy if you have any questions.