(This post contains the concept of Financial Independence & Retire Early (FIRE), and terms like 4% withdrawal rate that may sound confusing. If you like to know more, jump to the end of this blog post for more information.)

When we approaching June in New Zealand, you can see lots of personal finance articles tell everyone to put in some money into their KiwiSaver and get the free money. I want to focus on a group of people who is working toward financial independence and wants to retire early. They may think since they are planning to retire way ahead of 65, KiwiSaver is irrelevant to them. They could be in KiwiSaver, but not sure if they should include KiwiSaver as part of their financial independence plan.

Return on your KiwiSaver contribution

If you wish to live off your saving and investment, you ought to find the best return on investment out there. For KiwiSaver, your employer has to match your 3% contribution, and some employer may go higher. That’s 100% return on investment! (Correction: Actually is not 100% return because the employer needs to pay tax on their contribution. So the ROI is 100% – Tax, from 10.5%-33% less. Still a great return)

The government also provide KiwiSaver member tax credit for the first $1042.86 contribution from you each year (not counting your employer contribution). The Government will pay 50 cents for every dollar of member contribution annually up to a maximum payment of $521.43. That’s 50% return on your first $1042.

If your wife/husband/partner is not working and you are working full time, you should consider contributing $1042 into their account as well. Those credits are risk-free and guaranteed. It is hard to find such return on the market with basically no-risk.

Locked until 65

Some people think the big problem of KiwiSaver is you cannot access the fund until you turn 65 or to buy your first home. For the people who are planning an early retirement, they like to put every dollar into their investment so the investment can generate enough income to support their living expenses. They don’t count on KiwiSaver and NZ superannuation to retire. However, you should still put money into your KiwiSaver.

One simple question: Do you plan to live beyond 65? If yes, then you should contribute to your KiwiSaver because it’s your money! You will spend on your investment before 65, and you will still spend on your investment after 65. The KiwiSaver fund is just one of your investment funds, and you don’t draw on that fund before 65, it will still help you to achieve your financial independence.

Include KiwiSaver fund into your early retirement number

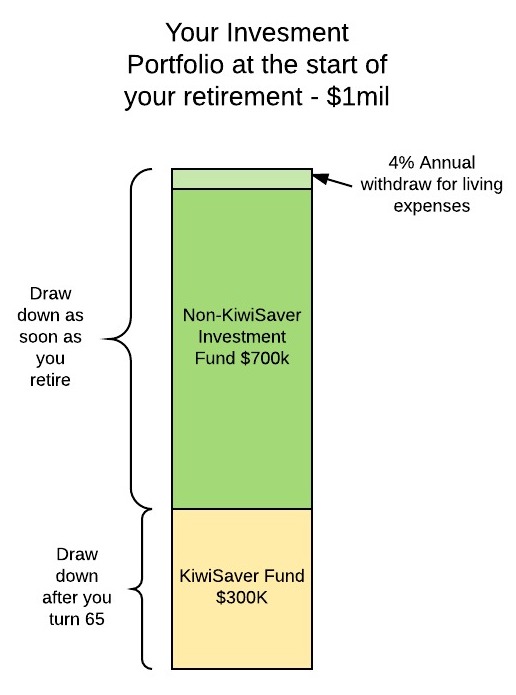

Look at the graph below. We assume you need 1 million portfolios to retire early, $300k in KiwiSaver and $700k in a normal investment fund. Your annual withdrawal rate 4%.

You just need to stack up your investment and put KiwiSaver at the bottom and only draw the fund at the top. You keep drawing your non-KiwiSaver investment fund before you turn 65 and let your KiwiSaver Fund untouched. Yes, your non-Kiwisaver fund may get smaller and smaller (depends on your withdrawal rate) because you are drawing $40K (4% of 1 million) on a 700k investment fund. However, your KiwiSaver fund will keep growing. When you reach 65, you can draw from both funds.

Therefore, you should keep contributing to your KiwiSaver and include KiwiSaver as part of your early retirement plan.

Don’t over contribute into KiwiSaver

The key is you should not put too much into your KiwiSaver. You don’t want your non-KiwiSaver fund run out of money before you reach 65. Although it’s unlikely but possible.

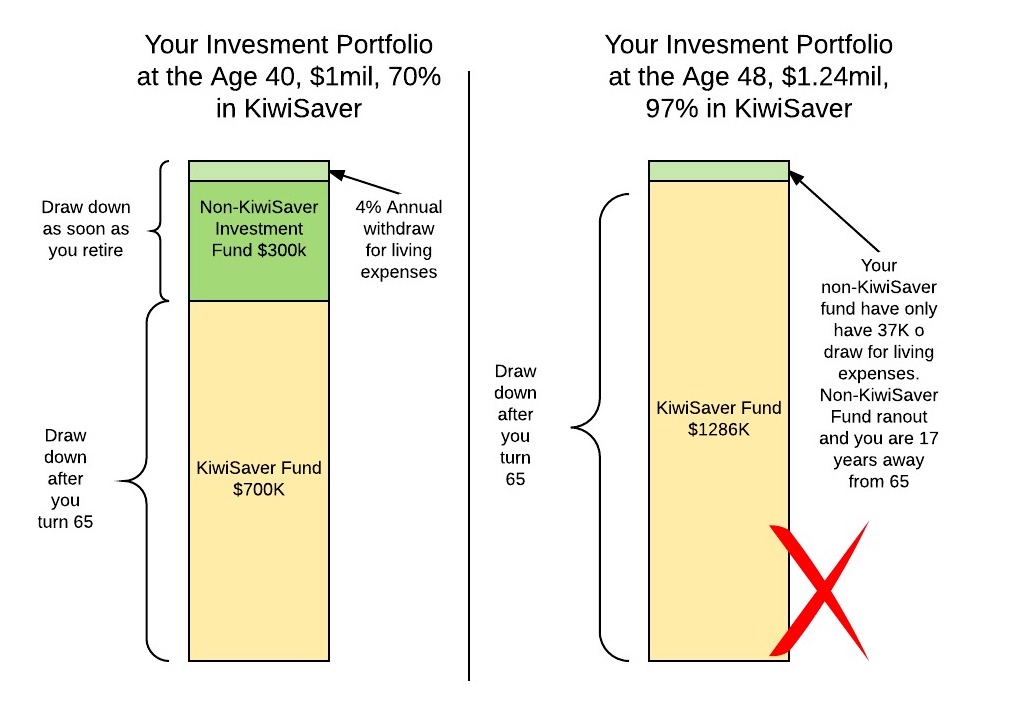

Let’s assume you are 40 years old and have 1 million investment portfolio. You plan to draw 4% on your investment every year for living expenses. The expected return on investment is 6%. However, for some unknown reason, 70% of your investment are in KiwiSaver, and only 30% of your investment are in non-KiwiSaver Fund. You can only draw from your non-KiwiSaver fund before you turn 65.

By age 48, your total portfolio growth to 1.24 million but your non-KiwiSaver fund ran out. Most of your money are locked in KiwiSaver, and you are 17 years away to access them. You need to go back to work.

To avoid that, you just simply contribute up to wherever your employer will match and enough to get the member tax credit every year. Put all extra cash into your non-KiwiSaver investment, including paying off mortgage, shares, bond, property, etc.

Now, if we reverse that situation and put 30% investment in KiwiSaver, 70% in non-KiwiSaver. That non-KiwiSaver fund will least 30 years. Here is the how the fund works.

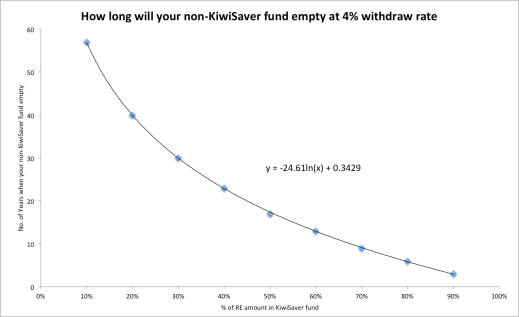

How long will you non-KiwiSaver fund least?

I actually worked out the formula on how many years your non-KiwiSaver fund will least base on percentage of your portfolio in KiwiSaver. The graph was based on 4% withdraw rate.

X is the percentage of your KiwiSaver and Y is the number of years will your non-KiwiSaver fund last.

If your Kiwisaver is about 18% of your total investment and you are 28, do you need to worry? Using that formula y = -24.61(0.18) + 0.3429, y =42.5. Your Non-Kiwisaver fund will least 42.5 years, by the time your non-KiwiSaver fund runs out, you are already 70 years old.

If you plan to retire at age 38, you will have to draw on your non-KiwiSaver fund for 27 years. Using that formula 27 = -24.61 In(x) + 0.3429, x = 33.85%. So your KiwiSaver needs to be less than 33.85% of your total investment portfolio.

That formula only works with 4% withdraw rate. You can work out how long will your non-KiwiSaver fund least with your own figure. Check out this google sheets. Make a copy and play around.

Conclusion

- KiwiSaver is a great investment with a high return on investment due to employer match and government tax credit. It is one of the best investment in New Zealand.

- You should contribute toward your KiwiSaver to achieve Finacial independence and include your KiwiSaver amount into your equation.

- Do not over contribute into your KiwiSaver.

- If you are employed, you should contribute up to your employer match and no more.

- If you are self- employed, just put in $1042.86 to get your $521.43 tax credit every year.

- All extra cash goes into non-KiwiSaver investment.

- If you are not retiring extremely early (in your 20s) and your KiwiSaver is below 20% of your total investment portfolio, you will be alright.

About FIRE

If you want to know more about Financial Independence & Retire Early, I will cover that in the future. Meanwhile, Check out the link below.

What is Financial Independence & Retire Early (FIRE)

The Shockingly Simple Math Behind Early Retirement

The 4% Rule: The Easy Answer to “How Much Do I Need for Retirement?”

Kiwi Mustachians – New Zealand FIRE community (Facebook Group)

Email thesmartandlazy@gmail.com or follow me on Twitter @thesmartandlazy if you have any questions.

{kind=link}